For the past three decades India's banking system has several outstanding achievements to its credit. The most striking is its extensive reach. It is no longer confined to only metropolitans or cosmopolitans in India. In fact, Indian banking system has reached even to the remote corners of the country. This is one of the main reason of India's growth process.

The government's regular policy for Indian bank since 1969 has paid rich dividends with the nationalisation of 14 major private banks of India.

The first bank in India, though conservative, was established in 1786. From 1786 till today, the journey of Indian Banking System can be segregated into three distinct phases. They are as mentioned below:

-

Early phase from 1786 to 1969 of Indian Banks

-

Nationalisation of Indian Banks and up to 1991 prior to Indian banking sector Reforms.

-

New phase of Indian Banking System with the advent of Indian Financial & Banking Sector Reforms after 1991.

Phase I

The General Bank of India was set up in the year 1786. Next Bank of Hindustan and Bengal Bank. The East India Company established Bank of Bengal (1809), Bank of Bombay (1840) and Bank of Madras (1843) as independent units and called it Presidency Banks. These three banks were amalgamated in 1920 and Imperial Bank of India was established which started as private shareholders banks, mostly Europeans shareholders.

In 1865 Allahabad Bank was established and first time exclusively by Indians, Punjab National Bank Ltd. was set up in 1894 with headquarters at Lahore. Between 1906 and 1913, Bank of India, Central Bank of India, Bank of Baroda, Canara Bank, Indian Bank, and Bank of Mysore were set up. Reserve Bank of India came in 1935.

During the first phase the growth was very slow and banks also experienced periodic failures between 1913 and 1948. There were approximately 1100 banks, mostly small. To streamline the functioning and activities of commercial banks, the Government of India came up with The Banking Companies Act, 1949 which was later changed to Banking Regulation Act 1949 as per amending Act of 1965 (Act No. 23 of 1965). Reserve Bank of India was vested with extensive powers for the supervision of banking in India as the Central Banking Authority.

During those days public has lesser confidence in the banks. As an aftermath deposit mobilisation was slow. Abreast of it the savings bank facility provided by the Postal department was comparatively safer. Moreover, funds were largely given to traders.

Phase II

Government took major steps in this Indian Banking Sector Reform after independence. In 1955, it nationalised Imperial Bank of India with extensive banking facilities on a large scale specially in rural and semi-urban areas. It formed State Bank of India to act as the principal agent of Reserve Bank of India and to handle banking transactions of the Union and State Governments all over the country.

Seven banks forming subsidiary of State Bank of India was nationalised in 1960 on 19th July, 1969, major process of nationalisation was carried out. It was the effort of the Prime Minister of India, Mrs. Indira Gandhi. 14 major commercial banks in the country were nationalised.

Second phase of nationalisation Indian Banking Sector Reform was carried out in 1980 with seven more banks. This step brought 80% of the banking segment in India under Government ownership.

The following are the steps taken by the Government of India to Regulate Banking Institutions in the Country:

-

1949 : Enactment of Banking Regulation Act.

-

1955 : Nationalisation of State Bank of India.

-

1959 : Nationalisation of SBI subsidiaries.

-

1961 : Insurance cover extended to deposits.

-

1969 : Nationalisation of 14 major banks.

-

1971 : Creation of credit guarantee corporation.

-

1975 : Creation of regional rural banks.

-

1980 : Nationalisation of seven banks with deposits over 200 crore.

Banking in the sunshine of Government ownership gave the public implicit faith and immense confidence about the sustainability of these institutions.

Phase III

This phase has introduced many more products and facilities in the banking sector in its reforms measure. In 1991, under the chairmanship of M Narasimham, a committee was set up by his name which worked for the liberalisation of banking practices.

Phone banking and net banking is introduced. The entire system became more convenient and swift. Time is given more importance than money.

In the past, farming was carried out in a traditional way. It was a subsidence farming and was more or less self sufficient Credit needs of the farmers were limited and were met with mostly by the money lenders, relatives, friends and to some extend by Taccavi loans from Government. Money lenders used to exploit the farmers in various ways like exorbitant rates of interest, false documents, etc.

After independence and particularly after the Green Revolution, agriculture entered the era of modernisation and the credit needs of the farming community started increasing. In the present day market oriented farming, the credit has become one of the crucial inputs.

A changing environment and government policies are forcing banks to lend more to the agricultural sector. Both private and public banks are now involving themselves in a lot of agri-based lending activities. Besides financing traditional activities, banks are also involved in training and setting up consultancies, agri clinics, the export and marketing of agricultural produce, etc.

Specialized loans (like horticulture, aquaculture, animal husbandry, floriculture and sericulture businesses) to meet specific needs of the farmers are offered by the banks. The Farmers can benefit from these loans by timely approach and prompt repayment.

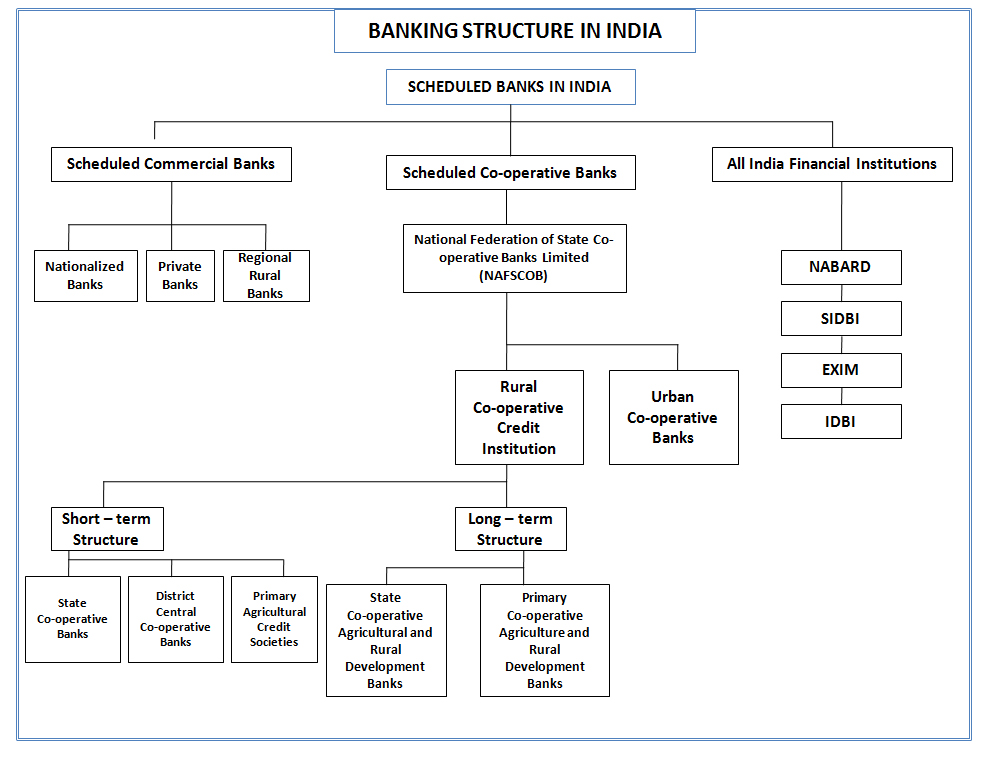

Click here to view Banking Structure in India

{kind=link}